4 Easy ways to deter fraud

Last month, the National Post published an article and story about how an accountant was able to buy $6M worth of Apple electronics without anyone noticing for 5 years. To understand why events like this still happen in today's business world full of automated tools & technology, it's important to understand the environments which allow fraud to germinate.

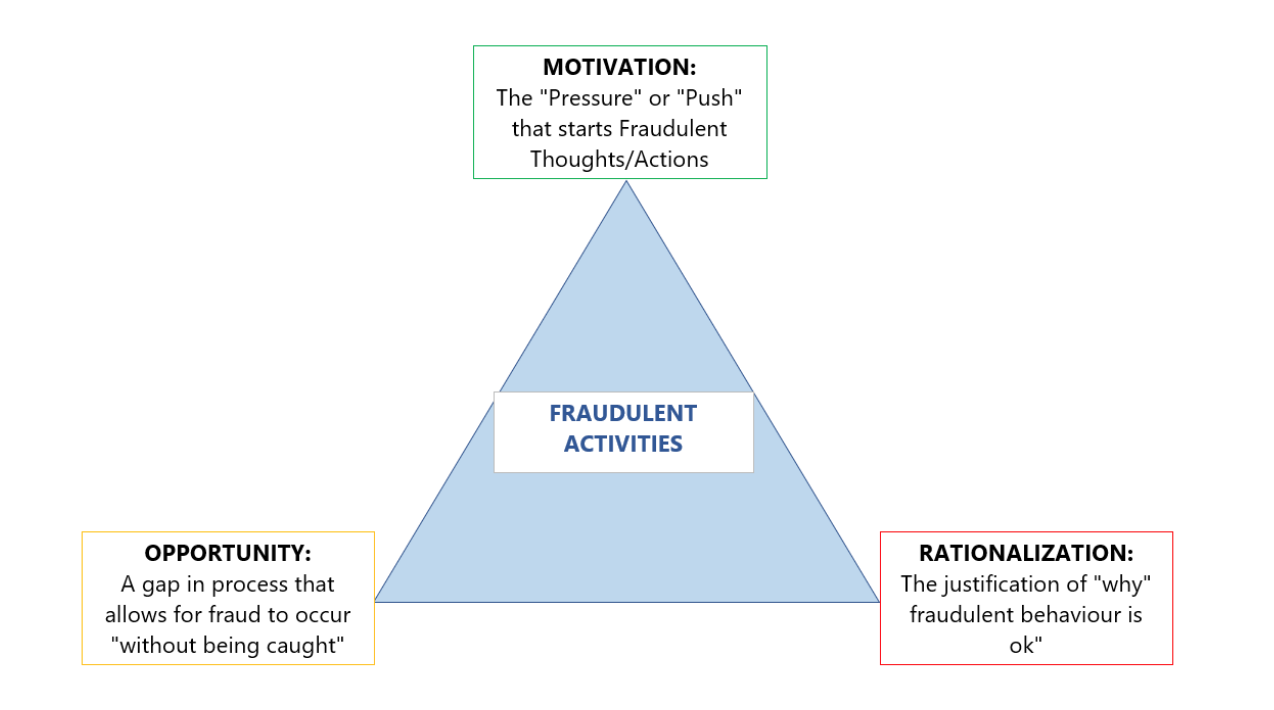

Fraud happens when three conditions are present:

1. Motivation

2. Opportunity

3. Rationalization

In the Accounting & Audit world, we call this the Fraud Triangle.

1. MOTIVATION:

You may be someone who is trained and educated in a specific discipline, but one day, something major changes in your life: circumstances are different, and you now have some pressure or stress.

The pressure can be internal or external.

Internally - maybe you just worked 3 months of overtime on a special project with no additional pay increase or recognition; perhaps you have just been passed up for a promotion and you think and feel "I'm worth than my boss knows", or "I deserve more".

Externally - maybe you've been overspending and bills are piling up; or someone in your family is ill with high medical bills; perhaps your spouse lost his/her job and there are mounting financial pressures to pay bills and maintain your lifestyle.

Such pressures and thoughts are enough to push you off the slippery slope and into realm of fraudulent behaviours unknowingly.

2. OPPORTUNITY:

Once the internal and/or external motivation exists, an opportunity has to present itself for someone to commit fraud. In this case, the Accounting Manager realized she reviews her own expense reports.

She probably tried once to expense a personal expense (maybe accidentally?) and then also recognized that no one noticed or flagged it.

The opportunity to "get away with it" is generally why people continue to commit fraudulent acts.

3. RATIONALIZATION:

Rationalization happens after the person knows s/he is committing fraud but justifies why it's "Ok" that s/he is doing it!

For eg. "Everyone is doing it" or "I'll return it later - I'm just borrowing for now" or my favourite, "If it were important enough, someone would review it".

While we may never know or agree with the true rationalization, we can speculate what the Accounting Manager in this story was justifying. She might have started with expensing just a couple of personal items and ramped up to bigger-ticket items because she probably rationalized, “because no one found the small items, they probably won't find these larger ones either!"

So, if you're a Business Owner, Divisional Manager or CEO, you are probably asking, "How could this have been prevented?"

Here are a few solutions that are quick and easy to implement that can give you and your management team some comfort that you are reducing any opportunities that breed Fraud:

1. SET POLICY

If employees know that there is a no tolerance policy for unethical and criminal behaviour, it can help deter individuals from falling off the slippery slope to begin with.

2. SEGREGATE APPROVING DUTIES & PROCESSING DUTIES

It's easy to approve your own work - it's never wrong!

Where possible, try to have different people do the record keeping and the approval of transactions.

In small companies, where resources are lean and segregation of duties can't always be established, the oversight and spot checks become more important!

3. OVERSIGHT: REPORT ON ACTUALS vs. BUDGET

The importance of Budgeting stands out in this case. Having a budget established and approved by different people on the Management team would have helped establish a baseline of what monthly, quarterly or annual spend would have been.

Independent of the daily processing and approving of expenses that the Accounting Manager was responsible for, her Manager could have reviewed Budget vs. Actuals and questioned any anomalies or differences.

The key here is REGULAR & FREQUENT review. It's also the reason why accountants always talk about month-end, Quarter-end or Year-End b/c those are frequent time periods to review certain financial data.

Don't underestimate how just asking follow-up questions or reviewing a report, can deter fraudulent activity, because you are demonstrating that there is oversight and therefore you are reducing the opportunity & rationalization for fraud to rear its ugly head.

4. FREQUENT SPOT CHECKS

As a follow-on from reviewing variances of Budgets vs. Actuals, it could be helpful to spot-check the details. Look for unusual purchases outside of your expectation (eg. New vendors or vendors that provide services that aren't typical for your industry, or large dollar amounts)

Stories like this highlight why it is important to have a strong internal oversight controls and frequent review of reports. We tend to rely on our (sometimes automated) systems to be able to alert us to problems, but strong internal oversight sometimes boils down to the human side of managing self and people. Sometimes fraud cannot be detected over time because there were instances of collusion and intent to conceal, but that is an article for another day…

If you have ever had success in using any of the solutions above, please share your experiences below or if you would like our D-Squared team to help review your internal controls or simply help your team set-up simple Budget vs. Actual data reports, feel free to contact us through the form on our website.